In a move that could transform the regulatory framework for corporate sustainability in the European Union, the European Commission has proposed delaying the implementation of the Corporate Sustainability Reporting Directive (CSRD) by two years and significantly modifying its requirements. The measure, which is part of the so-called “Simplification Omnibus Package”, seeks to reduce the administrative burdens imposed on companies by 25%, as stated in the official document, equivalent to an estimated saving of 40 billion euros.

If the reform is approved, the number of companies required to file sustainability reports would be reduced by 80%, as the threshold for CSRD application will increase from 250 to more than 1,000 employees. In addition, the elimination of sectoral standards and the elimination of more stringent audits will ease the requirements for companies that are still required to report.

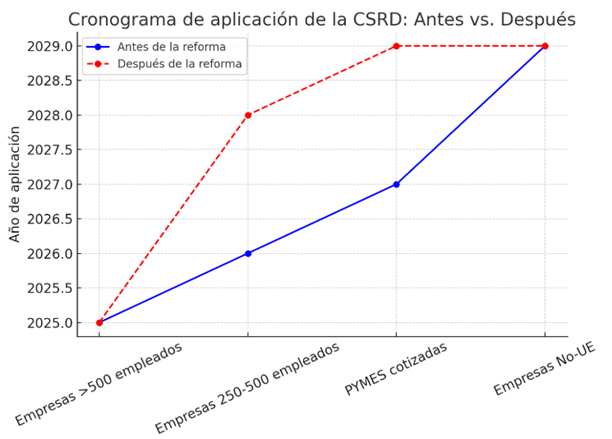

1. Keys to CSRD reform

Delay in deadlines:

- Second wave companies (more than 250 employees, less than 500) that were due to report in 2026 will now report in 2028.

- Third wave companies (listed SMEs and other entities) that were due to report in 2027 will now report in 2029.

- First wave companies (more than 500 employees) remain on the original schedule (report in 2025).

New definition of affected companies:

- Now only companies with more than 1,000 employees and that meet other financial criteria will report.

- Listed SMEs are eliminated from the scope of application.

Goodbye to sectoral standards:

- The Commission will not develop the sector-specific standards that were to be published in June 2026.

- Only general sustainability standards (ESRS) will be maintained.

Less audit burden:

- The possibility of increasing the audit requirement from “limited assurance” to “reasonable assurance” is frozen.

- Companies will only need limited validation of their reports.

- Another significant adjustment will be made to the Green Asset Ratio (GAR) for banks. As of the reform, financial institutions will be allowed to exclude exposures to smaller companies (less than 1,000 employees and 50 million euros in turnover) from the calculation of this indicator. This change is intended to improve the accuracy of the indicator without overburdening banks with information of low impact in terms of sustainability.

New voluntary standard for SMEs:

- A “VSME standard” will be implemented for companies outside the mandatory scope, with more flexible requirements.

- In addition to these changes to the CSRD, the Commission also plans adjustments to the EU Taxonomy. The option for companies to report activities partially aligned with the Taxonomy will be introduced, encouraging a gradual environmental transition. In addition, a financial materiality threshold will be established to reduce the administrative burden and reduce the length of reporting templates by 70%.

1.2 Impact on transparency and markets

The new rules will significantly reduce the amount of sustainability information available in Europe. According to Commission estimates included in the document, around 80,000 companies would be exempted from the reporting obligation.

This poses a risk to the availability of data in financial markets, as investors and banks could lose access to environmental and social impact information. A reduction in the integration of ESG factors in investment decisions is also expected.

To mitigate these effects, the Commission has announced the creation of a 100 billion euro fund for industrial decarbonization, with the aim of supporting the green transition without compromising business competitiveness.

2. CSDDD changes: Laxer due diligence and delayed implementation

In addition to the CSRD, the Corporate Sustainability Due Diligence Directive (CSDDD) will also undergo substantial modifications:

Companies’ liability is limited to direct suppliers (Tier 1):

- Companies will no longer be required to verify their entire supply chain.

- Only in exceptional cases, when there is clear evidence of irregularities, should they investigate beyond their direct suppliers.

Climate transition plans are reduced to a “check box exercise”:

- Companies will no longer be required to demonstrate concrete progress.

- The obligation to periodically review these plans is eliminated.

Weaker sanctions and lower legal liability:

- The fines that Member States can impose on companies that fail to comply are limited.

- The obligation to terminate contracts with non-compliant suppliers is eliminated.

Delayed implementation until 2028:

- The original deadline established the application in 2027 for companies with more than 5,000 employees.

- All implementation phases are now postponed for another year.

3. Reactions and political debate

Las modificaciones propuestas han desatado un intenso debate entre empresas, legisladores y grupos ambientalistas. Mientras que el sector empresarial y las cámaras de comercio celebran la reducción de costos y la mayor flexibilidad, argumentando que este alivio regulatorio fortalecerá la competitividad de las empresas europeas frente a sus rivales en EE.UU. y Asia, las organizaciones ecologistas y ONGs alertan sobre los riesgos que conlleva la disminución del alcance de la CSRD, advirtiendo que podría generar un “gran vacío de datos” en la UE.

On the other hand, the CBAM reform has also generated expectations in the commercial sphere. The introduction of an annual threshold of 50 tons for importers will exempt small market players from obligations, reducing bureaucracy without significantly affecting emissions coverage. In addition, stricter mechanisms will be implemented to prevent evasion practices and ensure the long-term effectiveness of this mechanism.

At the same time, some MEPs criticize that the reform weakens the CSDDD by limiting due diligence only to direct suppliers, which in their view renders it practically inoperative. The proposal will now have to be reviewed by the European Parliament and the Council of the EU, where it could still undergo modifications before final approval.

At ALL4, we are committed to providing our clients with the tools and knowledge necessary to comply with these standards and maximize their positive ESG and EHS impact. Our comprehensive approach helps companies navigate this new regulatory landscape, promoting responsible practices that strengthen the sustainability of their value chains.