The Task Force on Nature-related Financial Disclosures (TNFD) and the European Financial Reporting Advisory Group (EFRAG) have jointly published a guide that harmonises the European Sustainability Reporting Standards (ESRS) with the TNFD disclosure recommendations. This action highlights the remarkable overlap between the two frameworks, making it easier for companies to comply with the Corporate Sustainability Reporting Directive (CSRD). The collaboration, formalised through a Memorandum of Understanding (MoU), aims to ensure consistent and high quality sustainability reporting, providing accurate data for stakeholders and promoting sustainable development.

The high level of correspondence between the ESRS environmental standards beyond climate change (E2-E5) and the key recommendations and metrics of the TNFD is reflected, among others, in the following aspects:

Concepts and definitions: Both TNFD and ESRS recommend the need to disclose impacts, risks and opportunities related to nature, including dependencies on nature to the extent that they generate material risks.

Materiality approach: The ESRS requires disclosures to be based on the principle of dual materiality. The TNFD approach allows for different approaches to materiality, including the dual materiality approach required by the ESRS.

LEAP approach: TNFD developed the LEAP approach for economic actors to identify and assess their nature-related issues. The ESRS states that companies can conduct their materiality assessment on sustainability issues such as pollution, water, biodiversity and ecosystems, and the circular economy (all ESRS environmental standards beyond climate change) using the LEAP approach. The LEAP approach has been designed to help reporting organisations identify both impact materiality and financial materiality, providing a comprehensive approach for CSRD report preparers.

Reporting pillars: Both the TNFD recommended disclosures and the ESRS reporting areas are organised around the four disclosure pillars of the Task Force on Climate-related Financial Disclosures (TCFD): Governance, Strategy, Risk Management, and Metrics and Objectives.

Recommended disclosures and metrics: The 14 disclosures recommended by TNFD are reflected in the ESRS. Both the TNFD recommended disclosures and the ESRS requirements are designed to provide relevant and accurate information on sustainability issues related to nature. In addition, there is strong consistency between the key global disclosure metrics of the TNFD and the related metrics in the ESRS.

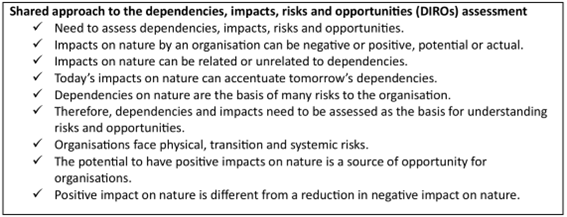

Common approach to the assessment of dependencies, impacts, risks and opportunities (DIRO):

Source: Task Force on Nature-related Financial Disclosures (TNFD) European Financial Reporting Advisory Group (EFRAG). (2024). Mapping of Correspondence to Align ESRS and Nature-related Disclosures. EFRAG.

Tony Goldner, CEO of TNFD underlined their commitment to transparency: ‘Many have asked us for further guidance to ensure that their reports comply with the mandatory CSRD requirements’.

EFRAG and TNFD will continue to support the disclosure of nature-related information, promoting transparency and sustainable development. For our part, at Laragon, we are committed to the effective implementation of the ESRS to continue to pave the way towards more sustainable and ethical business practices.